Thursday Trivia ~ The Rise of Quick Service Restaurants, Burger King IPO and Cafe Coffee Day wind up!

January 16, 2020Thursday Trivia ~ Mimetic Theory and How it impacts your Financial Future!

February 20, 2020

CAGR and XIRR are the most commonly used investment terminologies in the financial services industry while describing the investment returns to an investor. At times, an investor tends to get confused whether the two are same or carry some stark difference.

Let’s start by looking at the definitions.

Compounded Annual Growth Rate (CAGR)

(source: Investopedia.com)

Compound annual growth rate (CAGR) is the rate of return that would be required for an investment to grow from its balance in the beginning to its balance at the end of the tenure, assuming the profits were reinvested at the end of each year of the investment’s lifespan.

CAGR is nothing but the geometric mean of returns for all the years you stayed invested. So for to find out a CAGR for an investment over 10 years, one needs to find out annual returns of 10 years. Each annual return is then added by 1 and then multiplied to find out the Compounded Annual Growth Rate.

Extended Internal Rate of Return (XIRR)

XIRR or extended internal rate of return is a measure of return which is used when multiple investments have been made at different points of time in a financial instrument like mutual funds. It is a single rate of return when applied to all transactions (investments and redemptions) would give the current rate of return.

Surprisingly, the definition of XIRR is not given on Investopedia.

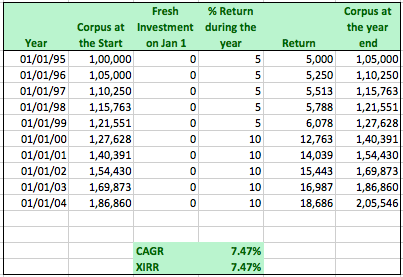

CAGR and XIRR will be the same in the case of a lump sum investment.

Scenario 1: Rs. 1 lakh invested at the beginning grows at 5% in the first 5 years and 10% in the next 5 years.

Scenario 2: Rs. 1 lakh invested at the beginning grows at 10% in the first 5 years and 5% in the next 5 years.

Observation:

A reader would notice that in these 2 scenarios, Mr. X’s investment of Rs. 1 lakh will generate the same amount of corpus after 10 years. Compounding at different rates for different time periods don’t have any impact since there are no cash flows.

CAGR and XIRR are same in both the cases.

Only difference is that in Scenario 2, the investment will compound at the faster rate in the first 5 years and in Scenario 1, investments will compound at a faster rate in the remaining 5 years.

CAGR and XIRR will be different when there are multiple cash flows due to which annual returns for each cash flow is variable.

A brief background

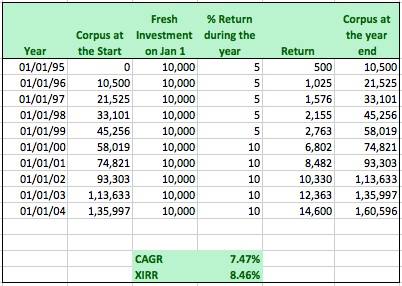

Extending on the context of above two scenarios, suppose Mr. X, an investor decides to invest Rs. 10,000 every year for a period of 10 years. In the first scenario, the investments grow at 5% in the first 5 years, then 10% in the next 5 years. In the second scenario, the investments grow at 10% in the first 5 years and then at 5% in the remaining 5 years. Here, we are trying to figure out whether the CAGR and XIRR will be similar or different in both the scenarios.

As part of the exercise, we recommend you to do a quick calculation in your mind as well.

Scenario 1: Investments grow at 5% in the first 5 years and then at 10% in the next 5 years.

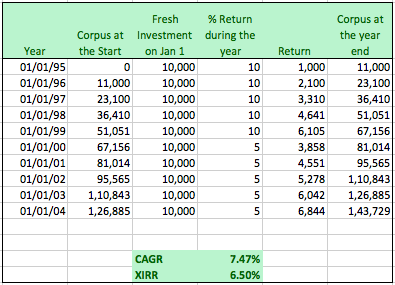

Scenario 2: Investments grow at 10% in the first 5 years and then at 5% in the next 5 years

Observation:

In the first scenario, Mr. X makes a decent Rs. 1,60,596 at the end of 10 years with an investment of Rs. 1 lakh. Whereas, in the second scenario, Mr. X makes Rs. 1,43,729 at the end of 10 years. A reader would observe here that the magic of compounding can lead to a better experience when the investments are compounded at higher rates towards the end of the tenure.

Whereas the interesting part here is that CAGR in both scenarios remain the same, in fact a reader would notice that CAGR has remained the same in all 4 scenarios, the reason for this is that CAGR is a geometric mean of returns and has nothing to do with cash flows during the period. Hence, a reader might feel that Mr. X will end with the same corpus because the CAGR is the same. That is clearly not the case.

Yet, there is a difference in XIRR. Sequence of returns matters, in case of recurring investments (or multiple investments).

How does an investor with a layman approach to finance looks at returns?

‘Returns’ is the most important part of conversation for any investor. The objective is simple; money should make more money. Let’s say for example, a person born in 1960s or 70s has a very different way to think about investment return. The conversation with such a person is pretty straight forward, he or she bought a house in 1990s worth Rs. 10 lakhs which today can be sold at Rs. 1 crore. In their conversation, Rs. 90 lakh is their investment return. No second thoughts. But if you ask a person who understands finance, he would take out his calculator, run some numbers and say it’s just 8% Compounded Annual Growth Rate (CAGR) in a period of 30 years.

Since, a lot of investors tend to use CAGR for a house since they look at point to point investment returns as there is no cash flow in between.

In case of investments in mutual funds for instance, an investor tends to have multiple cash flows in the form of Systematic Investment Plans (SIPs) or partial redemptions for different periods of time. At such a time, an investor can calculate CAGR for each SIP which will be for a different duration at a different rate than other SIPs or XIRR can be simply used to ascertain the investment returns for the same.

In a nutshell, an investor should look at XIRR when there are multiple cash flows and returns generated. But in case of point to point investment, CAGR can also be looked at since the XIRR too will remain the same.

– Saurabh Mittal and Jinay Savla